Check your credit score for free!

Discover smart financial solutions tailored to your needs. Whether it's balance transfers, loan consolidation, or flexible top-ups, we've got you covered.

What is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. In India, credit scores range from 300 to 900, with higher scores

indicating better creditworthiness. The Credit Information Bureau (India) Limited (CIBIL) is one of the primary credit bureaus in India that

calculates these scores.

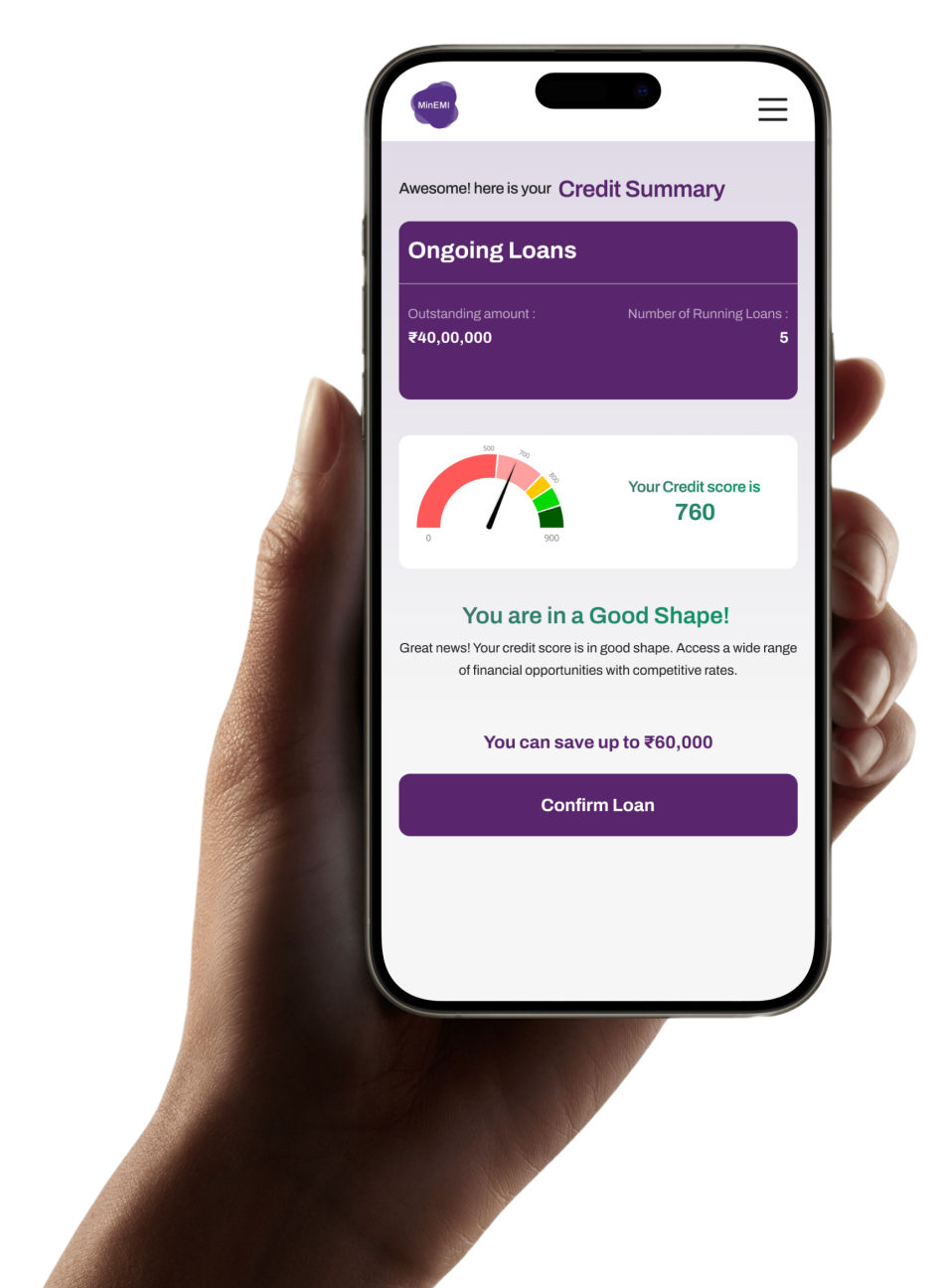

Why is a Good Credit Score Important?

A good credit score, typically above 750, can lead to:

Easier Loan Approvals: Lenders are more likely to approve loans for individuals with high credit scores.

Lower Interest Rates: Borrowers with excellent credit scores often receive loans at lower interest rates.

Higher Credit Limits: Credit card issuers may offer higher credit limits to individuals with strong credit histories.

Building a Credit Score with No Credit History

If you have no credit history, consider the following steps to build your credit score:

Apply for a Secured Credit Card:

These cards are backed by a fixed deposit and can help establish credit history.

Become an Authorized User:

Being added to someone else's credit card account can help you build credit.

Take a Credit-Builder Loan:

Some financial institutions offer loans specifically designed to help build credit.

Use Credit Responsibly:

Make small purchases and pay off the balance in full each month to establish a positive payment history.

Factors Affecting Your Credit Score

Several factors influence your credit score:

Payment History: Timely payments boost your score, while missed or late payments can significantly lower it.

Credit Utilization Ratio: This is the ratio of your current credit card balances to your credit limits. Maintaining a low ratio (preferably below 30%) is beneficial.

Length of Credit History: A longer credit history provides more data on your financial behavior, which can positively impact your score.

Credit Mix: A diverse mix of credit accounts, such as credit cards, mortgages, and personal loans, can favorably affect your score.

New Credit Inquiries: Frequent applications for new credit can be seen as risky behavior and may lower your score.

Check Your Cibil Score Without

Impacting Your Credit Score

Tips to Improve and Maintain Your Credit Score

Pay Bills on Time: Consistently paying your bills by the due date is crucial.

Reduce Outstanding Debt: Aim to pay off existing debts to lower your credit utilization ratio.

Limit New Credit Applications: Apply for new credit only when necessary to avoid multiple hard inquiries.

Maintain Old Credit Accounts: Keeping older accounts open can lengthen your credit history, which is beneficial.

Monitor Your Credit Report: Regularly review your credit report to identify and dispute any inaccuracies.